NAV rate in November was 106.24, which gives an increase for the month of 0.57 (0.5394%). It's a good month, the fund is progressing according to plan. I see a NAV of 6.5-7.0% by the end of the year, given the information I have today.

Inflow of SEK 98 million, many thanks for that.

New lending in November was small. We are well balanced with inflows and new lending.

I am now being asked how inflation affects our credit funds and how rising interest rates affect them.

Assume an inflation rate of 3% and a return of 2%, then the value of that investment decreases by 1% at an annual rate in current money value. This is the case with most bond funds that invest in publicly traded corporate bonds. Our credit funds, which this year yield from 5% to 7%, on the other hand, give a real increase in capital of 2% to 4% at an annual rate.

Furthermore, with regard to the general interest rate situation.

Our credit funds are subject to IFRS9, which means that they are valued at book value with a hypothetical market valuation that can only be adjusted downwards. We therefore cannot write up the value when interest rates fall, as funds with market-listed holdings do. The reverse applies to a general interest rate increase, then we do not need to write down the value of our holdings. It is the credit quality that determines the value of the holdings. When interest rates rise, we can reinvest matured loans and new capital at higher interest rates, which is positive for the return on the fund.

I return to the fact that you as investors must first and foremost assess our ability to provide relevant credit assessments and manage the risks that come from this. As an investor, you avoid the volatility of market movements and get a very high risk-adjusted return.

We continue our work with extra frequent follow-up of our companies with regard to the Corona situation.

The market

We've seen a messy November for risky assets. This is where our funds are at their best in your portfolios. We deliver a month with a stable return, regardless of whether it bounces in all directions or edges on other markets.

My assessment is that the new virus variant was a trigger on something that had been building up for some time. Stock markets have risen despite inflation concerns and then only a catalyst was needed to initiate a sell-off with accompanying turbulence.

Where do we go from here and what do we have to consider?

· Inflation

· New viruses

· Liquidity

· Turn of the year

· Geopolitical risks

· Energy prices

· Monetary policy

· And so on

I don't intend to go through these but just want to give you a hint of what I'm looking at among other things.

I would like to conclude by thanking you for your trust as an investor in the fund and wishing you a Merry Christmas and a Happy New Year.

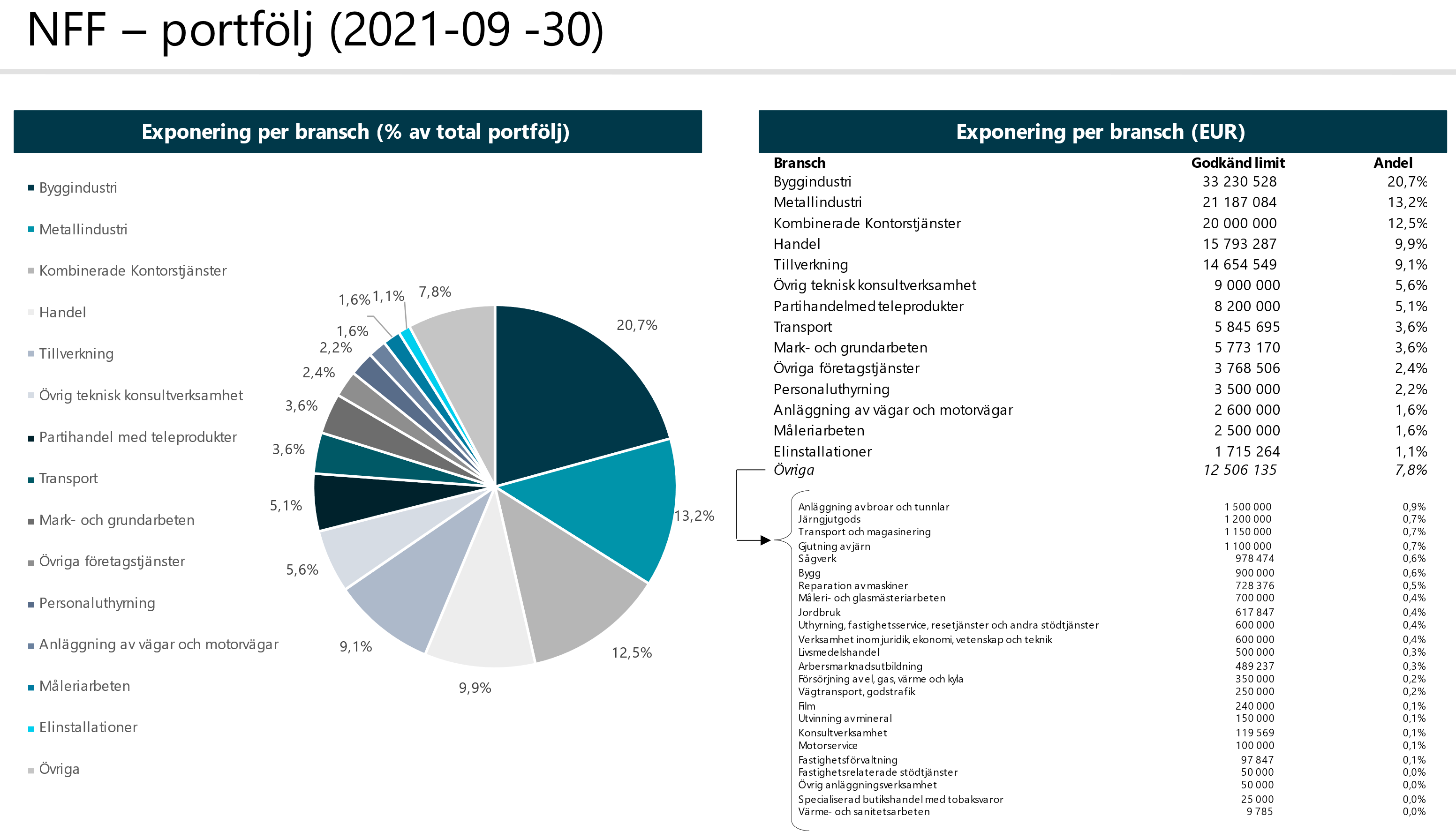

Below you can see how the fund is invested

We have introduced quarterly liquidity in the fund for redemption on 2021-07-01, we maintain monthly investment opportunity. Redemption must be notified at least 90 days before redemption.

We continue our work with extra frequent follow-up of our companies with regard to the corona situation.

Finserve Nordic, which is the fund's AIF manager, has in 2020 joined the company to the PRI network, Principles for Responsible investment. The network is independent but supported by the UN and encourages investors to invest responsibly by following the principles developed by the network.

All funds under Finserve's management follow the responsible investment process formalized in Finserve's Sustainability Risk Integration Policy. The policy is available on the company's website https://finserve.se/viktig-information/. Each fund's sustainability policy is available on the funds' websites

When you do your analysis of the fund, you should primarily look at the credit risk and the liquidity risk in the fund. Are you comfortable with the credit risk that the fund's holdings generate? Furthermore, the assets are illiquid and it can take some time to get back your investment if many people want to withdraw deposited funds at the same time. The fund has a low market risk and has a low correlation with other asset classes.

We emphasize that we are not stressed by non-loaned funds, but continue to work based on our models for credit assessment, all to ensure a good diversification of the portfolio in relation to the credit risk we take.

If you need to sell your holdings, do it in the primary market, where you will get the best price.