NAV rate in September was 105.10, which gives an increase for the month of 0.54 (0.52%) It's a perfectly ok month, the fund is moving according to plan.

It was a 30 day month so that makes a couple of basis points on NAV. Inflow of SEK 44 million, many thanks for that.

New lending in February was approximately SEK 150 million. We continue our work with extra frequent follow-up of our companies with regard to the Corona situation. Maybe it's time to redefine this sentence?

We have a methodology with more frequent follow-up that we implemented in connection with Covid and we will continue with it, also post Covid.

The market

We have experienced unrest in the world's stock markets during September.

Driven by concerns about future inflation and thus rising bond yields. Furthermore, above all, the FED is talking about cutting back on support purchases of bonds and future interest rate increases.

Evergrande, the Chinese real estate company, is also causing global concern. The state authorities learned an expensive lesson in connection with Lehman and I don't think the Chinese state will let the company go under completely. However, it will sting and sting in some portfolios before the smoke clears. The price of Evergrande's bonds has fallen into bankruptcy status. The bond market expects a default and that the assets are worth approx. 25% in the event of a bankruptcy today (see graph below). After all, the Chinese government has tightened credit for a few years and now we see very clearly what can happen when highly leveraged companies can no longer get hold of cheap loans.

Can it happen in Sweden?

In the graph below you can see the expected P/E ratio, S&P 500 actual price and expected earnings per share in the S&P 500.

As you can see, we are at levels that we last saw in connection with the IT crash in 2000. It is then perhaps not so strange that a certain correction is taking place. How deep and long it will be, we will only know afterwards. However, it is very much in the hands of how the central banks manage their monetary policy, support purchases of bonds and the rhetoric regarding inflation.

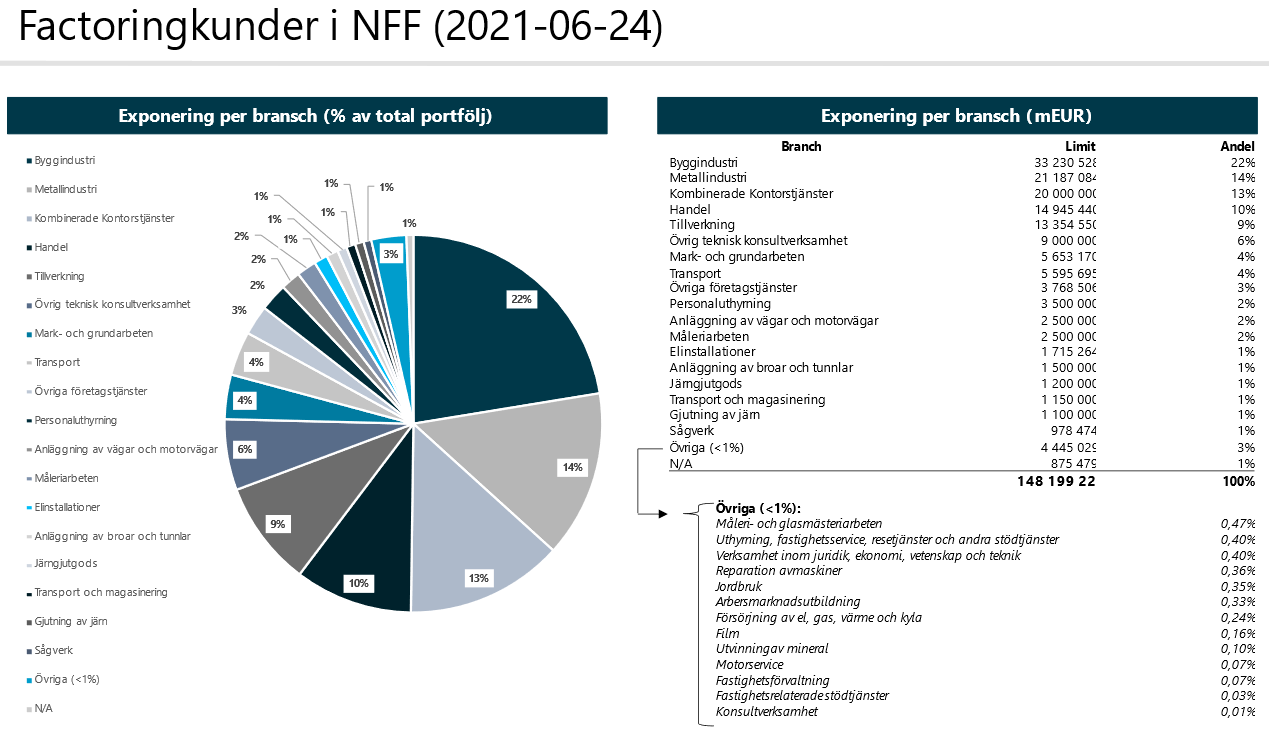

Below you can see how the fund is invested. Although the image is a couple of months old, the distribution is the same, so it illustrates the distribution well.

We have introduced quarterly liquidity in the fund for redemption on 2021-07-01, we maintain monthly investment opportunity. Redemption must be notified at least 90 days before redemption.

We continue our work with extra frequent follow-up of our companies with regard to the Corona situation.

Finserve Nordic, which is the fund's AIF manager, has in 2020 joined the company to the PRI network, Principles for Responsible investment. The network is independent but supported by the UN and encourages investors to invest responsibly by following the principles developed by the network.

Finserve Nordic believes that the integration of sustainability risks is an important part of the funds' investment processes. Sustainability risks are defined as environmental, social, or corporate governance-related circumstances that could have a significant negative impact on the value of investments.

Social aspects include e.g. human rights, labor rights and equal treatment. Environmental aspects are e.g. the companies' impact on the environment and climate. Corporate governance aspects are e.g. anti-corruption, shareholders' rights and business ethics

All funds under Finserve's management follow the responsible investment process formalized in Finserve's Sustainability Risk Integration Policy. The policy is available on the company's website https://finserve.se/viktig-information/. Each fund's sustainability policy is available on the funds' websites.

The fund's AUM is less than the granted limits of approx. SEK 1.5 billion. This compilation does not come straight out of the system without a lot of manual work so it will not be included every month. It will be interspersed with the usual compilation.

(the fund uses its ability to leverage, hence the positive and negative allocation numbers)

When you do your analysis of the fund, you should primarily look at the credit risk and the liquidity risk in the fund. Are you comfortable with the credit risk that the fund's holdings generate? Furthermore, the assets are illiquid and it can take some time to get back your investment if many people want to withdraw deposited funds at the same time. The fund has a low market risk and has a low correlation with other asset classes.

We emphasize that we are not stressed by non-loaned funds, but continue to work based on our models for credit assessment, all to ensure a good diversification of the portfolio in relation to the credit risk we take.

If you need to sell your holdings, do it in the primary market, where you will get the best price.

If you are in a hurry to sell, the secondary market may be an option. The official NAV rate is published on the first banking day of each month, what is shown during the month on NGM is not, I want to stress, not always the official NAV rate, as fund shares may have been traded in the secondary market at a different rate than the official NAV.