NAV rate for February was 101.08, an increase on the month of 0.48 ( 0.477%) and a standard deviation of 0.91. The reason why we dip below 0.50 is a short month that makes about 3.5 points and some currency hedges that did not move in parallel across all maturities. In total, about 7 points in February. The latter return when they approach maturity.

We have inflows of around SEK 33m, thank you for that.

New lending in February was insignificant, this is because cash was limited in February. We have a robust pipeline so new money will come to work in March.

We continue our work with extra frequent follow-up of our companies with regard to the Corona situation.

Norway is tough in its shutdown of the economy and we monitor our holdings there extra closely.

The market

Inflation, that's the big issue. For those of you who follow us, you have read that I have been warning about inflation since last summer. It can arise from the enormous support that comes partly from fiscal policy and partly from monetary policy. These supports are absolutely right, however, they can have consequences and one that is desirable in a controlled form is inflation. History teaches us that inflation, if it really occurs, is rarely controlled. This is what the market has now opened its eyes to and is worried about. The central banks are clear that regardless of whether there is inflation and it shoots above the target, the zero interest rate will remain. That reasoning is now visible in the pricing of the 10-year bond in the US, the interest rate has practically doubled in a few weeks. It's from low levels but still a doubling, it's a very big move.

Do we need to be afraid that risky assets will take a lot of beating?

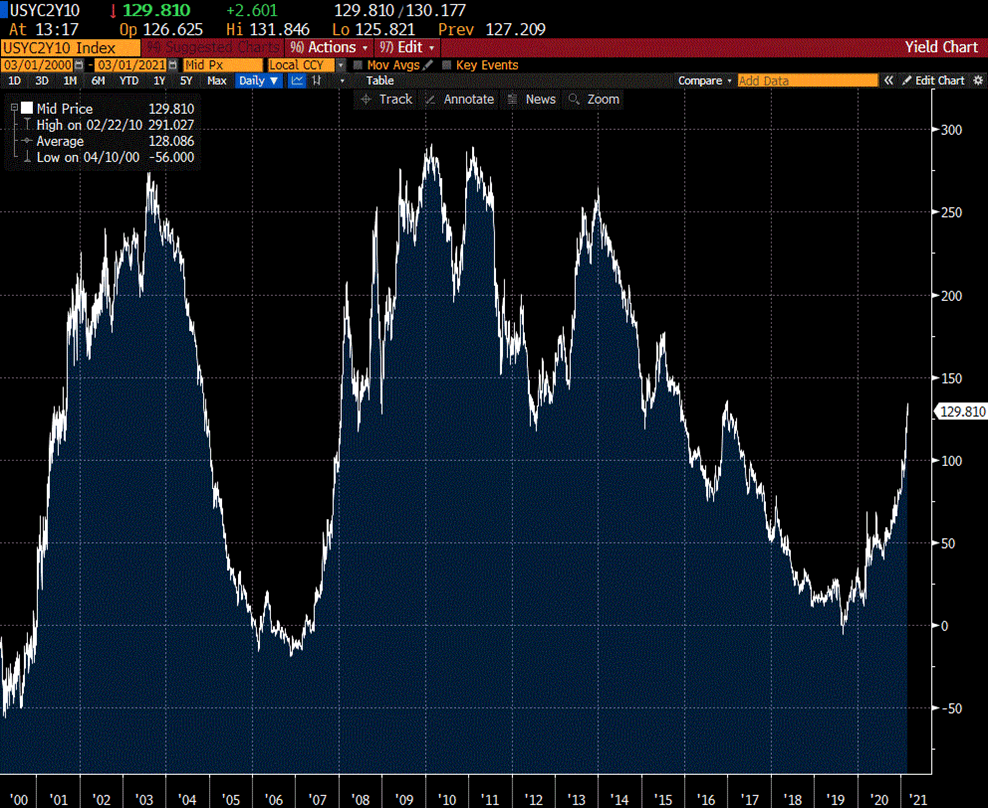

In the graph below, you can see the difference between the 10-year interest rate and the two-year interest rate in the US over the last 20 years.

The slope has been significantly greater than what we see today, so from that side we don't need to be terribly worried. However, I am sure that the difference will be greater in a year than it is today. The era of exceptionally low bond yields is behind us. A healthy inflation trend need not be bad for risky assets. What worries me is that many stock markets are at "all time highs" or close to them and credit spreads are at rock bottom. Companies that a year ago could barely issue HY bonds can today do so at interest rates that they could only dream of a couple of years ago. This leads me to believe that the continuation of 2021 may be volatile and we will see sharp swings ahead in many markets.

In comparison to funds that invest in market-listed high-yield bonds, we comply with IFRS 9 and only make adjustments in the valuation when called for by credit events. This means that from a market risk perspective the risk in SCF I is small, it is the credit risk you should focus on as an investor.

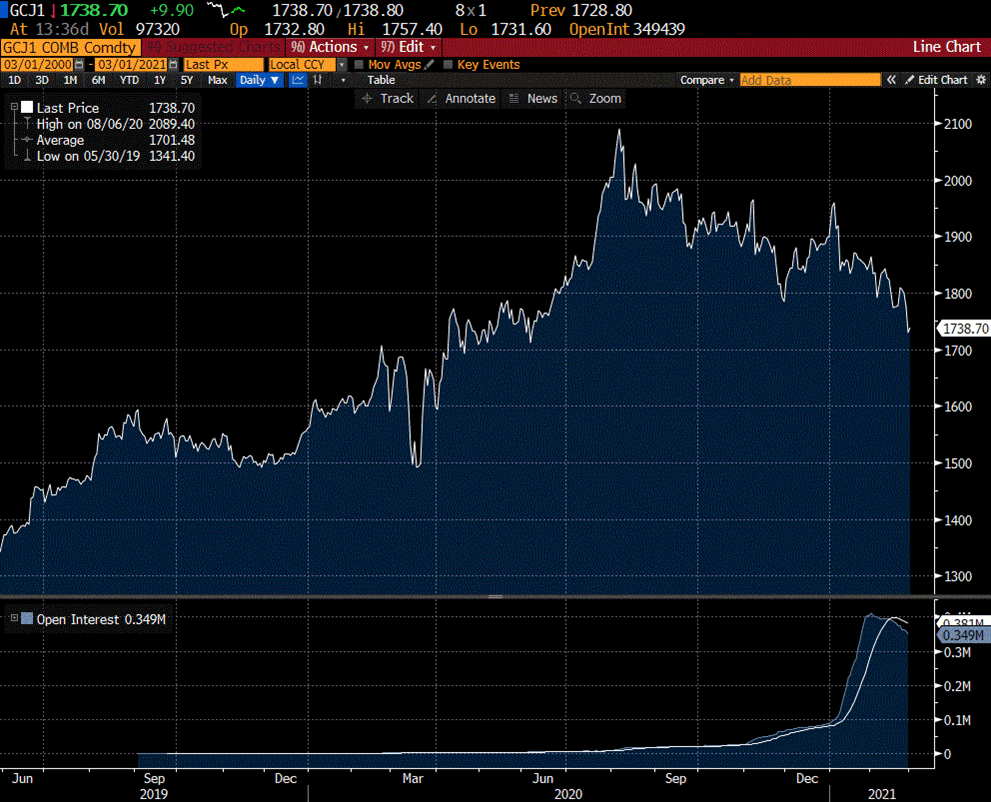

A paradox regarding inflation expectations is that the price of gold has not gone up in this environment, is it possible that those who are afraid of inflation have invested in cryptocurrencies instead? Or is inflation a non-issue?

This graph shows the price of gold over the last 2 years, instead of going up now the price has fallen recently while the market has focused on inflation.

We emphasize that we are not stressed by non-loaned funds, but continue to work based on our models for credit assessment, all to ensure a good diversification of the portfolio in relation to the credit risk we take.

If you need to sell your holdings, do it in the primary market, where you will get the best price.

At present, when the fund has delayed redemption and if you are in a hurry to sell, the secondary market may be an alternative. The official NAV rate is published on the first banking day of each month, what is shown during the month on NGM is not, I want to emphasize, not always the official NAV rate, as fund shares may have been traded in the secondary market at a different rate than the official NAV.