The recent escalation between Iran, Israel, and the United States has been characterized by a series of highly targeted strikes against Iran’s most critical military, nuclear, and energy infrastructure, alongside the elimination of several senior figures within the Iranian leadership. U.S. and Israeli operations have focused in particular on degrading Iran’s strategic capabilities, including reported strikes on the Natanz nuclear facility using bunker-penetrating munitions, as well as attacks on key energy assets such as the South Pars gas field, marking a notable expansion of the conflict into the economic domain.

At the same time, the campaign has involved a decapitation strategy aimed at Iran’s political and military leadership. Several high-ranking individuals have been reported killed, including senior figures within the security establishment such as the head of the Supreme National Security Council, the commander of the Basij paramilitary forces, and the country’s intelligence minister, alongside multiple IRGC commanders and senior officials. These losses are widely seen as an attempt to disrupt decision-making structures and reduce Iran’s ability to coordinate both domestic control and external military responses.

Can Iran still pose a threat?

The key question now is whether Iran still retains the capacity to pose a meaningful threat despite the extensive degradation of its infrastructure and leadership. Iran attempted to strike the U.S.–U.K. military base on Diego Garcia, roughly 4,000 kilometers from Iranian territory, marking a significant escalation in both intent and capability. While the attack ultimately failed, with one missile breaking apart mid-flight and another intercepted, the attempt itself is strategically important. It indicates that Iran is willing and able to project force far beyond the Middle East, targeting critical Western logistics hubs rather than purely regional adversaries.

What is particularly notable is the type of system likely used. Analysts assess that the missiles were probably derived from the Khorramshahr family and may have been modified to extend their range by reducing payload weight. At the same time, there is increasing speculation that Iran may be leveraging technology from its space program, such as launch vehicles like Simorgh, to enable longer-range ballistic trajectories. This crossover between civilian space launch systems and military missile development has long been suspected, but the Diego Garcia attempt suggests it may now be operational.

Equally important is the question of remaining missile stockpiles. Pre-war estimates suggested that Iran possessed on the order of 2,000 to 3,000 ballistic missiles across various ranges, with production capacity allowing for relatively rapid replenishment. While a significant number have already been fired in the current conflict, and U.S. and Israeli strikes have targeted storage sites and launch infrastructure, reducing daily launch capacity materially, Iran’s continued ability to sustain missile attacks indicates that its arsenal remains substantial.

Pressure on allies' missile stockpiles

At the same time, the conflict is increasingly exposing a different constraint, not Iran’s offensive capacity but the limits of allied defensive stockpiles. According to Rheinmetall CEO Armin Papperger, the war has rapidly depleted interceptor inventories across the West and the Middle East, with stockpiles now “empty or nearly empty” and at risk of being exhausted entirely if the conflict continues at the current intensity (Euractiv, 2026).

This dynamic reflects a structural imbalance in modern warfare, where relatively cheap Iranian drones and missiles force the use of highly expensive interceptor systems such as Patriot and other air defence missiles, each costing several million dollars. In the opening phase of the war alone, allied forces expended thousands of precision munitions and interceptors, far exceeding the pace seen in previous conflicts and raising serious concerns about sustainability over a longer time horizon.

The scale of incoming attacks illustrates why these stockpiles have come under such pressure. Iran has launched more than 1,200 ballistic missiles and over 2,100 drones across the region, targeting both Israel and multiple Gulf states. The United Arab Emirates stands out in particular, having faced over 1,600 drone attacks and more than 300 ballistic missiles, making it one of the most heavily targeted countries due to its role as a key hub for U.S. military infrastructure. Other states, including Qatar, Bahrain, Kuwait, and Jordan, have also absorbed significant volumes of attacks, highlighting the regional breadth of the conflict rather than a purely bilateral confrontation with Israel.

Source: Wikipedia (2026)

Taken together, this underscores that the war is not only being fought on the battlefield but also in industrial capacity and supply chains. While Iran’s arsenal is being gradually degraded, its ability to deploy large volumes of relatively low-cost systems continues to impose disproportionate pressure on Western and allied inventories.

Escalation risks and strategic uncertainty

The risk of further escalation remains high, although some recent signals point to a temporary slowdown in the most aggressive scenarios. President Trump has backed down from earlier threats to attack Iran’s energy infrastructure after what were described as constructive discussions. However, Tehran has publicly denied that any such talks took place, creating further uncertainty.

This has led to speculation that any dialogue may not involve the current official leadership, but rather alternative power centers within the Iranian system. Such dynamics could point to factions within the regime, or parallel structures, seeking engagement with the West. In more speculative scenarios, this has even been linked to the exiled crown prince Reza Pahlavi, with some suggesting that the U.S. could be exploring pathways to support a political transition in Iran with backing from internal actors. These remain highly uncertain and unverified developments, with limited visibility in actual decision-making channels.

On the escalation front, Iran has issued explicit warnings that any direct strikes on its power infrastructure would trigger retaliatory attacks against desalination plants in neighboring Gulf states. These facilities are critical for civilian water supply across much of the region, and any disruption would have severe humanitarian consequences. Saudi Arabia has already signaled that such an attack would constitute a red line and would likely draw it directly into the conflict militarily.

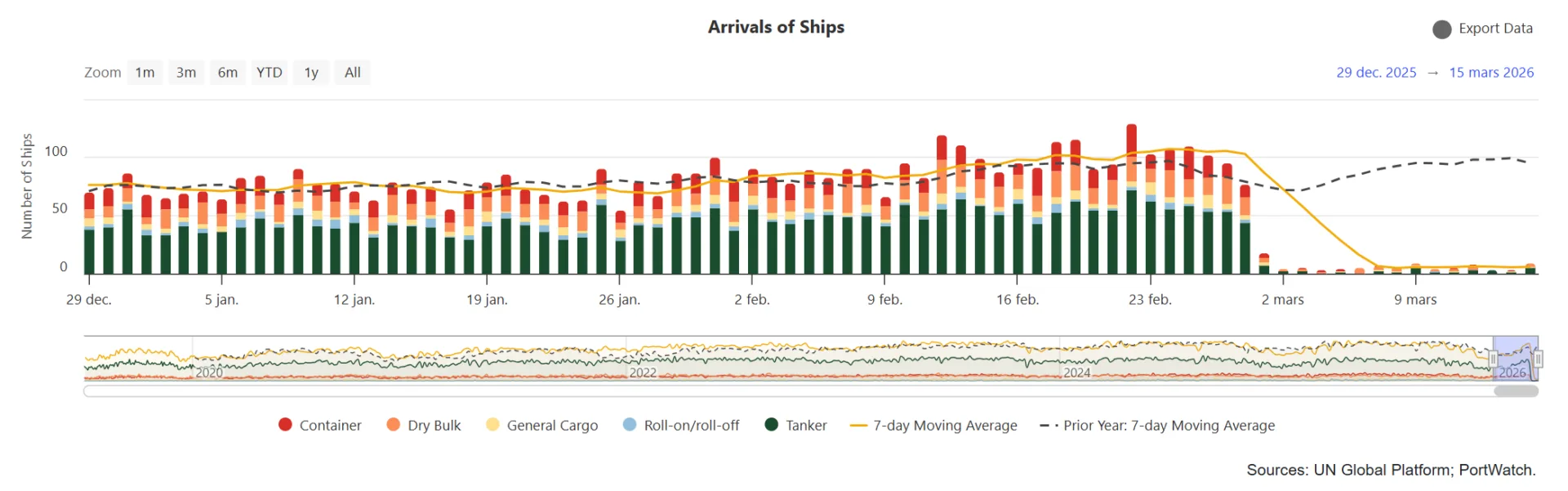

Beyond this, a further escalation scenario would likely center on the Strait of Hormuz, a chokepoint for global energy flows. Iran has historically relied on asymmetric tactics in the area, and a renewed escalation could involve the deployment of naval mines or other disruptive measures aimed at commercial shipping.

Links to the war in Ukraine

The conflict is also beginning to intersect with the war in Ukraine, both operationally and politically. There are increasing indications that Iran may be receiving intelligence support from Russia, in a manner broadly comparable to the real-time battlefield intelligence the United States has provided to Ukraine. Such cooperation could enhance Iran’s targeting capabilities, improve coordination of missile and drone strikes, and increase the survivability of its remaining systems.

At the same time, the U.S. has repeatedly called on European allies to contribute more actively to operations related to the Iran conflict, but responses have so far been limited. European leaders have emphasized caution, with EU foreign policy chief Kaja Kallas noting that “there is no broad support for putting personnel at risk in the region,” highlighting the reluctance to escalate militarily (EFN, 2026).

This divergence risks straining the transatlantic relationship at a time when cohesion is already under pressure. Trump has openly criticized European leaders, referring to them as weak and unwilling to step up, further deepening political tensions. Looking ahead, this could have structural implications for NATO once the Iran conflict de-escalates. One scenario is that the U.S. reduces or even withdraws support for Ukraine, shifting the burden entirely onto European countries. Another, less likely but still conceivable outcome, would be a more unilateral U.S. strategy, escalating support in Ukraine while simultaneously distancing itself from European partners.

Meanwhile, Ukraine has reportedly contributed personnel with battlefield experience, particularly in countering Iranian-made drones, to support U.S. operations in the current conflict. This may be interpreted as a gesture of strategic alignment and goodwill, although it remains too early to draw firm conclusions about how this will shape longer-term alliances or commitments.

Market and portfolio implications

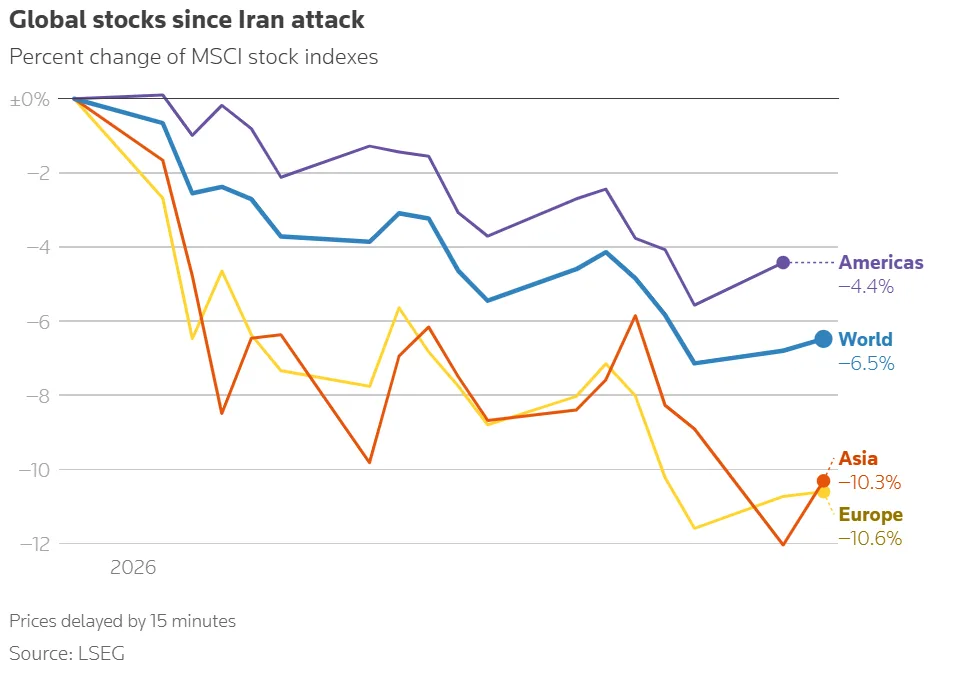

The financial market implications have been immediate and pronounced. Since the onset of the conflict, global equity markets have turned increasingly volatile, with most major indices down approximately 4 to 10 percent at the time of writing. The primary driver has been the effective disruption of the Strait of Hormuz. This has led to a sharp increase in oil prices and, more importantly, a repricing of geopolitical risk.

In the short term, this translates into higher overall market risk, including elevated energy costs, rising inflation expectations, increased uncertainty around central bank policy, and a clear deterioration in risk appetite across equity markets. This combination is typically negative for the broader market.

For our portfolio, the implications are more nuanced. A higher oil price is not directly positive for most companies within the Global Security Fund. However, for the majority of our holdings, oil itself is not the primary driver of performance. The key exception is companies with meaningful exposure to commercial aviation, such as Airbus and Safran, where higher fuel costs can weigh on demand and margins.

For the rest of the portfolio, what matters more is what the oil price represents, namely a signal of increased geopolitical friction, heightened focus on defense capabilities, energy security, and the resilience of critical infrastructure. These are core themes within our investment universe and are structurally reinforced in the current environment. In addition, the intensity of the conflict, particularly the extensive use of missiles and drones as discussed earlier, drives demand for the underlying systems, components, and technologies that many of our portfolio companies are exposed to.

We are closely monitoring developments and, should the current trajectory persist, we will continue to reduce exposure to segments that are more sensitive to higher oil prices, particularly within commercial aerospace. At the same time, a large part of the portfolio has demonstrated resilience and, in several cases, outperformance during the recent market downturn. Going forward, we expect to be more active in reallocating capital towards positions that are increasingly relevant in this evolving geopolitical landscape.