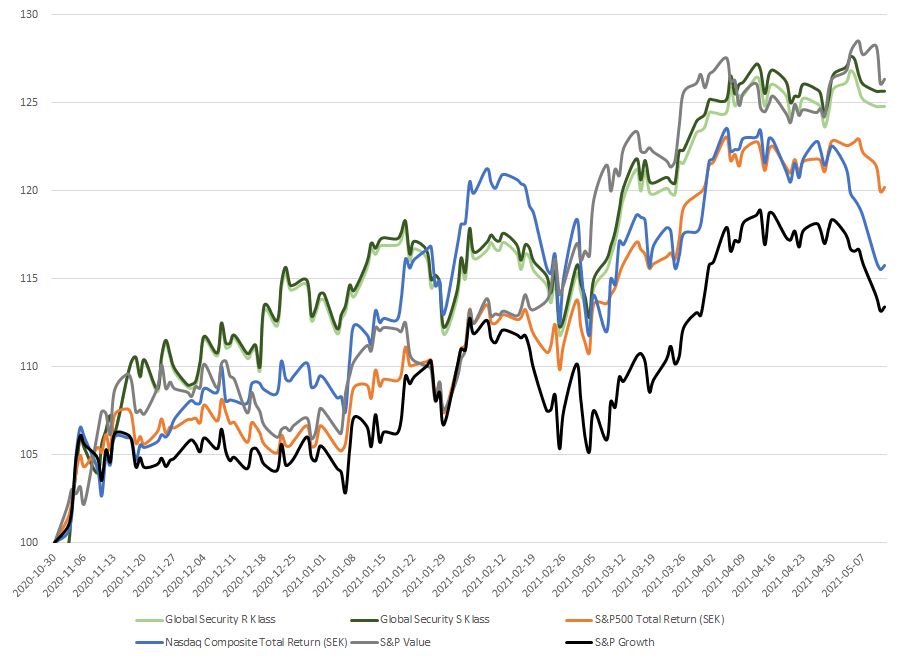

July was a strong month for global equity markets. The fund (R class) was up 1.5 % for the month.

Inflation data has continued to come in high, but the market still interpreted the latest FED statement positively and as less hawkish than previous statements. Inflation and the FED's actions are judged to be the most significant for the markets. The FED does not consider the US to be in a recession regardless of the technical definition, due to the fact that economic activity and growth have not declined on a sufficiently broad basis and especially not the labor market. The employment rate and new job creation are also what the FED will follow primarily in their goal of being data dependent to support their actions.

It is also interesting that the 10-year interest rate fell from its highest level of 3.5 % to 2.6 % during July and perhaps the inflation risk has been deemed to have decreased somewhat. Interest rates are of great importance for the valuation of IT companies, and these have had a good development during July as a result.

The reporting period for Q2 ended in July and there was great uncertainty around the big tech giants and their results and guidance going forward. The results of the reports from the FAANG companies were mixed with Meta (Facebook) and Google being quite weak while Amazon or at least parts of Amazon contained positive news and Microsoft had positive guidance going forward. These reports nevertheless brought relief to the stock market and mitigated the risks on the downside somewhat as there were concerns that they could indicate severely subdued economic growth.

The development of the dollar is interesting to follow as a strong dollar hits tech giants and their sales, especially EUR, YEN & CAD, where for example Microsoft is vulnerable.

We see the fund's exposure to cyber security as very interesting, but the fund's holdings in the sector, especially those companies with private individuals and or companies as buyers, will likely be drawn into the macro picture and the development of large IT companies, which can mean a lot of volatility. An interesting holding to highlight in cyber is CACI international, where the US government is one of the main customers. The company's share has had a positive development both YTD and in the 1-month term, and has generally shown less cyclical sensitivity.

After the reporting period, we see that the supply chain problem as a result of the corona pandemic remains within the defense sector, which in the short term affects total revenues for, among other things, the defense giant Lockheed Martin, but the sector as a whole continues to see good development. The geopolitical situation has been further strained in connection with Nancy Pelosi, the speaker of the US House of Representatives, visiting Taiwan. In connection with the visit, China has carried out extensive exercises. The Fund is of the view that geopolitical tension between the US and China is of a completely different dignity than the significant tension between Russia and the US. The fund's defense companies have exposure to developments, of particular interest is the fund's holdings in Huntington Ingalls Industries, maker of boats for the US Navy, which is up 9 percent over the past month and beat Q2 expectations.

The fund's top holdings during the month were Boeing and Cisco on a relative size basis, but also Honeywell, Crowdstrike and Leidos all contributed 25bps and above to the month's NAV. Boeing reported below expectations and is also having difficulty keeping up with Airbus's development and growth. At the same time, the view is that profits can increase and that the company becomes powerful when new products come out. The worst performance on a relative basis was SAAB and Raytheon. Both companies reported a below-expected profit, especially in terms of profit, but for Raytheon, forward growth in relation to the industry as a whole may also have been important.